Financial Modeling for Distressed Firms

As a company starts to experience financial difficulties, be it through increasing debt, declining profitability or a liquidity crunch, the roles of finance professionals shift. Rather than focusing just on growth, analysts and treasury managers are dealing with uncertainty, creditor relations and testing scenarios in a negative environment. This is where distressed company financial modeling skills are crucial. It’s a skill that combines hard numbers with practical judgement and for junior to mid-level practitioners, it’s one of the most rewarding and stimulating of corporate finance specialities.

Distressed company modeling is a far more urgent activity than financial modeling of firms in general. While a typical model may forecast revenue growth over a five-year period with conservative downward scenarios, a distressed model must take into account a shorter time frame, limited cash flows and even the prospect of bankruptcy or restructuring. Analysts need to know how to preserve cash, assess debt covenants, and model various scenarios of business turnaround – sometimes all at once. There is a lot at stake, and getting the assumptions wrong can have significant impacts for the company and its shareholders.

This article offers an overview of financial modeling in distressed situations. This includes the modeling approach, the importance of risk management and treasury management, using sensitivity analysis and scenario analysis to inform business decisions under distress and the lessons that can be learned from restructuring case studies. Whether it’s your first time developing a distressed financial model or you are simply seeking to improve your skills in this area, this article provides some practical techniques you can take away and apply today.

Understanding the Distressed Firm Environment

The first step in creating a model is to understand the financial environment of the distressed firm. Distressed firms are different from their healthy counterparts in that they may only have a short amount of time – weeks or months – before a liquidity event. Among the signs of distress are persistent operating losses, defaults on covenants in credit agreements, negative working capital, and the inability to meet debt obligations with operating cash flows. The initial challenge for an analyst in a distressed situation is to determine what the firm’s runway is to a liquidity event.

It’s important to distinguish between liquidity and solvency distress. Liquidity distress implies that while the long-term business may be sound, the company doesn’t have cash for the immediate short term. Solvency distress suggests that even if a firm had liquidated all of its assets, its liabilities would be greater than its assets. This has implications for all areas of the model – from cash flow forecasting to restructuring scenarios. In reality, these two types of distress often co-exist, and disentangling these two phenomena is a data-driven analysis that requires high-quality data.

The role of these factors is apparent in real life. In 2017, when Toys ‘R’ Us declared bankruptcy, it was easy to see that the business was making enough retail sales, but was crushed by the debt (US$ 5 billion) it owed from a leveraged buyout. The company was, in parts, a viable business, but it had an unsustainable capital structure. The difference between this and a good distressed model is that a distressed model would have identified the imbalance years ago, allowing the creditors and management to have the information they need to work out a restructuring before it was too late.

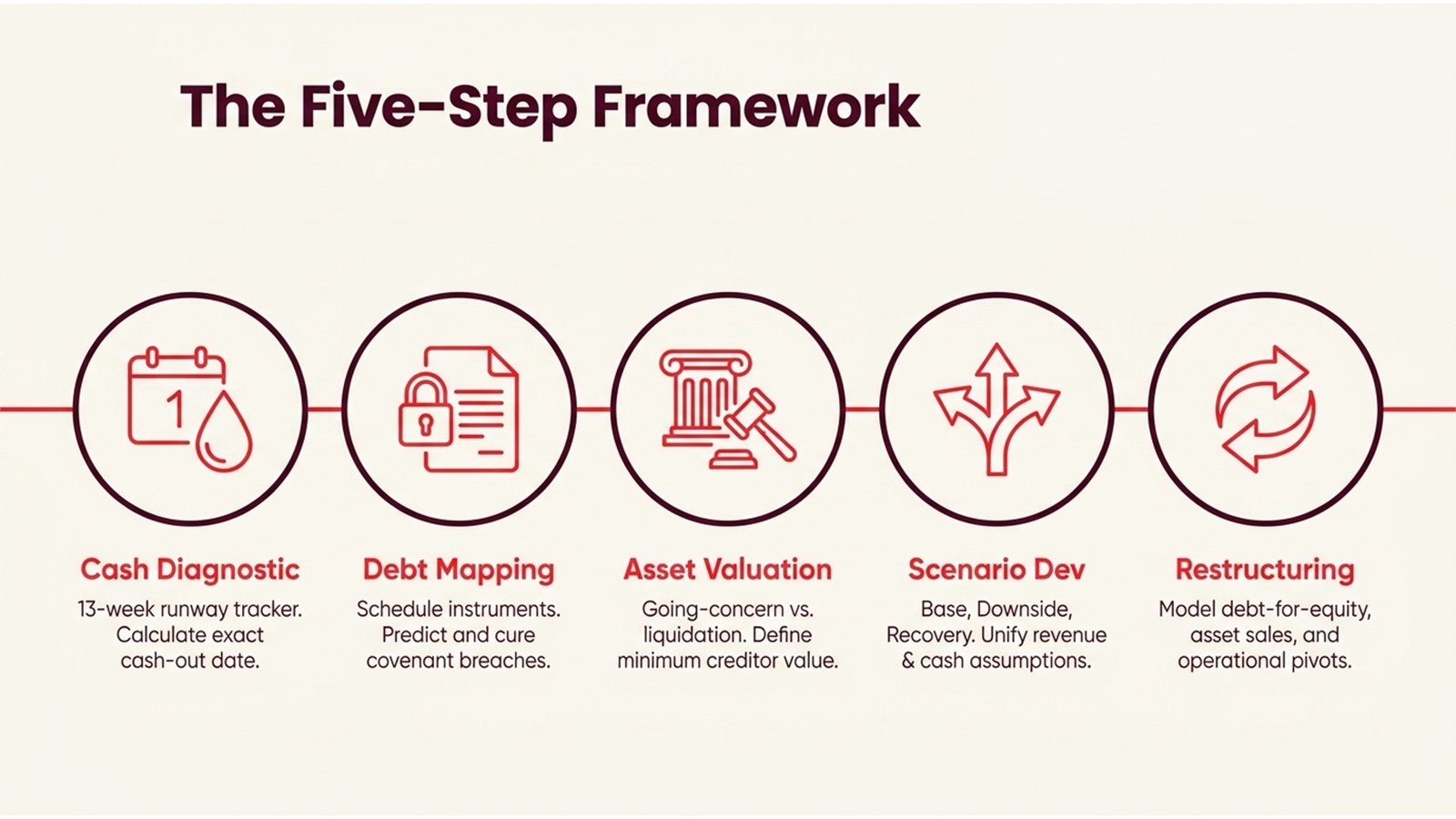

The Five-Step Framework for Distressed Company Financial Modeling

A model for distressed companies must be disciplined and adhere to a process. The five-step approach outlined below offers a useful roadmap for any financial model for a distressed company, from data collection to information for decision-making.

Process Flow 1: Five-Step Distressed Modeling Framework

| Step | Description |

| Step 1 | Cash Flow Diagnostic – Track cash in and out for the next 13 weeks. Determine the exact date the company will run out of cash with the current burn rate. |

| Step 2 | Debt and Covenant Mapping – Draw up a schedule of all debt instruments, their term, interest payments, and covenants. Identify potential breaches in the coming months and the effects of cure strategies. |

| Step 3 | Asset Valuation – In a standalone valuation of the key assets, assess the going-concern and liquidation value of the assets. This defines the minimum value to creditors. |

| Step 4 | Scenario Development – Develop at least three scenarios: base, downside and recovery. All scenarios must have consistent revenue, cost and cash flow assumptions. |

| Step 5 | Restructuring Scenario Modeling – Assess and model financial scenarios of specific restructuring proposals, such as debt-for-equity swaps, asset sales, or operational restructurings. |

The 13-week cash flow model is particularly important as it is the first type of model required by creditors and advisers in crisis situations. The 13-week cash forecast is different from longer-term models in that it models cash flows (customer receipts, wages, rent, interest, and debt service) rather than earnings. This level of detail highlights the critical cash issues facing a business: which creditors must be paid to keep the company afloat, which customer orders can be rushed through, and what level of cash cushion exists before the company must seek assistance.

The debt and covenant mapping exercise often highlights risks that aren’t apparent from a company’s financial statements. Lending agreements often contain maintenance covenants to restrict leverage ratios, interest coverage ratios, or to maintain minimum levels of liquidity. As a company moves towards a covenant breach, the lenders are given powerful leverage and the distressed model needs to consider the legal and financial effects of that power shift. This early warning and waiver or amendment modelling provides a guide to management’s negotiations with lenders.

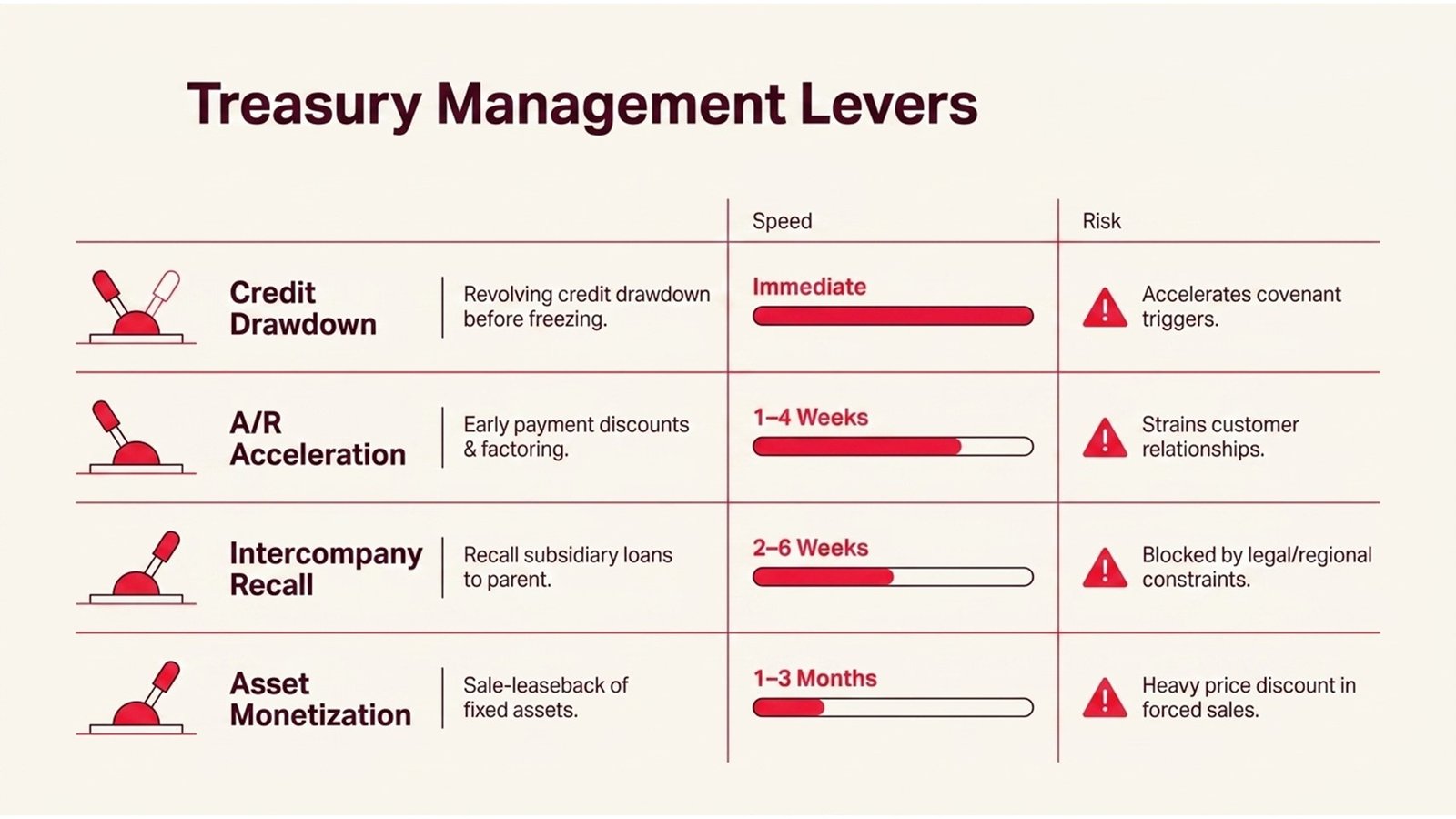

Risk Management, Treasury Management, and Liquidity Optimization

In a distressed situation, the treasury department is the business’s operations control room. While treasury departments in non-distressed firms are concerned with maximising the return on cash balances and managing foreign exchange risk, the focus in a distressed treasury management scenario shifts to preserving cash, communicating with stakeholders, and keeping the bankers on side. Risk management and treasury management in this situation involve a number of measures: cash pooling, delaying payments to vendors, speeding up cash collections from customers, and drawdown management of existing credit facilities.

Perhaps the biggest mistake in treasury management in distressed situations is not giving due consideration to intercompany cash flows in the group context. When the parent is distressed, subsidiaries might have a lot of cash, but the inability to upstream that cash (due to regulatory constraints in the local country, minority shareholder protection or ring-fenced financing structures) means the cash may not be available. In a model, such legal and structural restrictions need to be explicitly considered or the group’s liquidity position will be misleading.

With the restructuring of Sears Holdings in 2018 and 2019, for example. The firm’s treasury department was unable to quickly convert its valuable real estate assets into cash to meet short-term needs. The difference between book value and cash on hand – the typical risk management (and treasury management) failure – hastened the journey to bankruptcy. For modelers, this event serves as a reminder of the need to separate the value of assets from the value of liquid assets and to test the timing of the assets’ liquidity plan.

Table 1: Common Treasury Levers in a Distressed Scenario

| Lever | Mechanism | Typical Timeframe | Key Risk |

| Accounts Receivable Acceleration | Provide discounts for early payment or factoring | 1–4 weeks | Customer relationship strain |

| Supplier Payment Deferral | Agree on longer payment dates with suppliers | 2–8 weeks | Risk of supply issues if too long |

| Asset Monetization | Sale-leaseback of an asset | 1–3 months | Price discount in a forced sale |

| Credit Facility Drawdown | Revolving credit, draw down before freezing | Immediate | Accelerates covenant triggers |

| Intercompany Loan Recall | Recalls loans to subsidiaries to the parent | 2–6 weeks | Legal restrictions may apply |

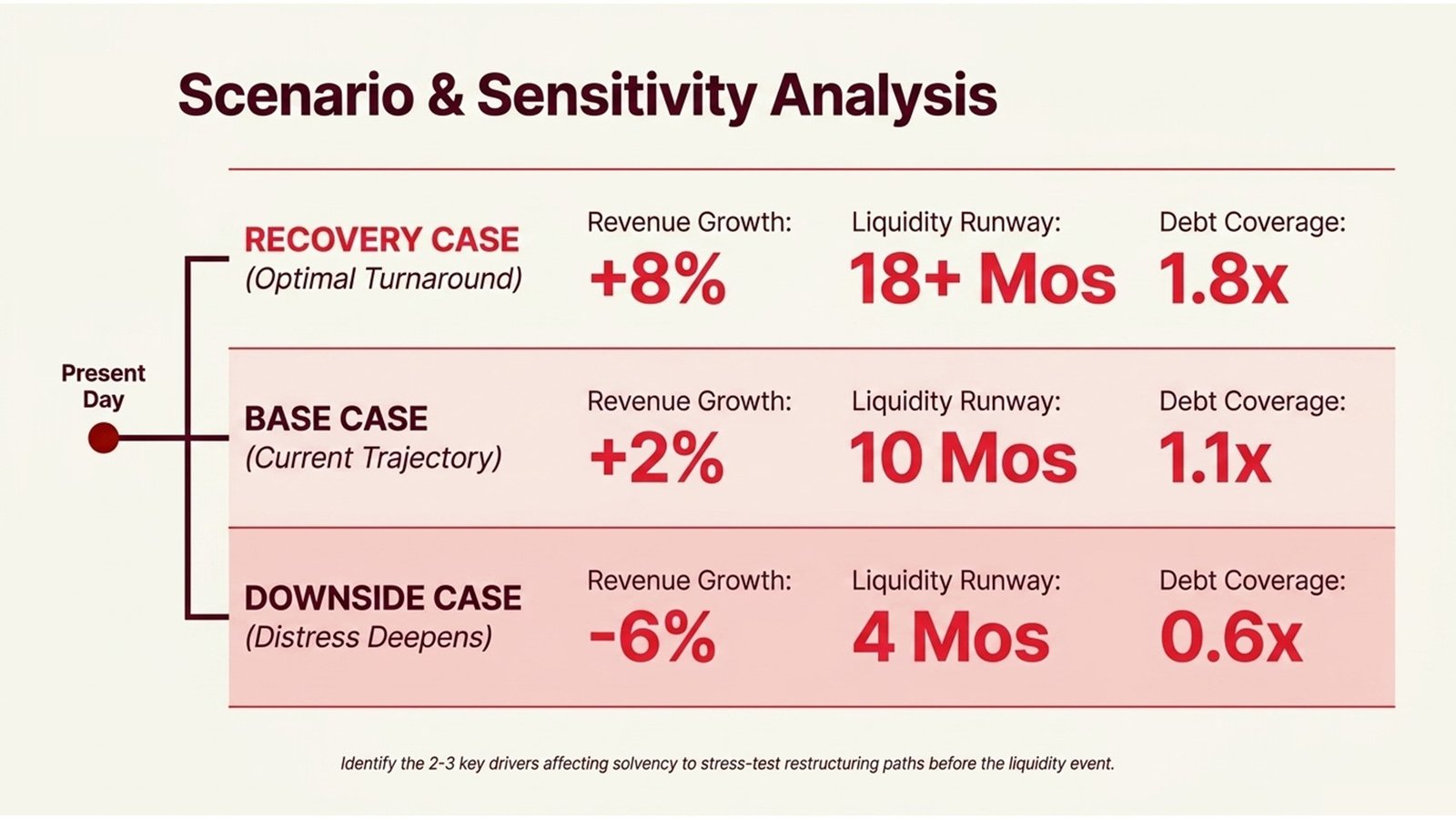

Scenario and Sensitivity Analysis Under Stress

The distressed environment requires multiple forecasts. The future is unknown, and there are many possibilities. As a consequence, scenario and sensitivity analysis are not a desirable but essential component of modeling. A good scenario analysis requires management and creditors to identify the key drivers of value and understand how the results vary as the drivers move in the wrong direction. It also helps them to test the robustness of the restructuring plan.

In reality, scenario and sensitivity analysis of distressed companies should be conducted around the two or three key factors that affect liquidity and solvency. For a retailer, these could be like-for-like sales growth and gross margin. For a manufacturer, it might be raw material costs and revenues. For an investment company, it could be occupancy rates and capitalisation rates. The model can then use these variables and a range of assumptions to create a decision matrix that advises managers and advisors of which restructuring options are still on the table for each scenario.

An example of effective scenario analysis is that of energy company Weatherford International. In 2015-2016, when oil prices tanked, management and advisors at Weatherford developed a range of scenarios and sensitivity analysis models to determine what oil price would make various debt structures untenable. That work helped guide its eventual out-of-court debt exchange in 2016, and when prices collapsed again, its prepackaged bankruptcy in 2019. The years of work in advance afforded management options not otherwise available.

Process Flow 2: Building a Three-Scenario Distressed Model

| Stage | Action |

| Define Key Drivers | Select 2-3 drivers that have the biggest impact on cash flow and solvency (e.g., sales, margin, capex). |

| Set Scenario Boundaries | Create best case, worst case and recovery case for each variable with rationale. |

| Build an Integrated Model | Integrate the income statement, balance sheet and cash flow statement to automatically update all scenarios. |

| Stress Liquidity Runway | In each scenario, calculate the number of months of cash and the earliest covenant breach date. |

| Evaluate Restructuring Paths | Identify possible restructuring options (debt reduction, equity raise, asset sale) in each scenario. |

| Present Decision Matrix | Summarise the results in a table that presents key results for each scenario for management and creditor consideration. |

Table 2: Illustrative Scenario Assumptions for a Manufacturing Firm

| Assumption | Recovery Case | Base Case | Downside Case |

| Revenue Growth (Year 1) | +8% | +2% | –6% |

| Gross Margin | 34% | 29% | 24% |

| Working Capital Days (Net) | 45 days | 55 days | 70 days |

| Capex (% of Revenue) | 4% | 3% | 2% |

| Months of Liquidity Runway | 18+ months | 10 months | 4 months |

| Debt Service Coverage Ratio | 1.8x | 1.1x | 0.6x |

Challenges, Lessons Learned, and What the Best Models Get Right

Those who have been through the fires in distressed situations identify a number of common issues. First is the quality of the data. Many distressed firms have weak finance functions, which means that the data to build the model (such as accounts receivable aging, inventory levels, intercompany balances) may be missing, wrong or simply not at the level of detail needed. The challenge when making assumptions in these circumstances is the need for both critical analysis and a healthy dose of distrust.

The second ongoing issue is the human aspect of distressed modeling. Distressed management teams are generally optimistic, both because they believe in the fundamentals of the business and because they do not want to acknowledge the dire situation they’re in. So the analyst or advisor is often confronted with the challenge of preparing a distressed model that is worse than the views of management. Knowing how to do this: how to clearly present the analysis; how to stick with the numbers; how to be open to different opinions – is something that can only be learned with experience.

The most valuable insight of any restructuring experience is that time is always in short supply. The best financial modeling of distressed companies does not react to problems as they arise. It spots the signs and quantifies the decline, and provides the information needed to take action before it is too late. Firms such as Kodak, which filed for Chapter 11 in 2012 after years of obvious distress, are examples of what not to do when it comes to financial modeling. The best models are proactive, multifarious, and dynamic – not reactive and rushed, when the horse has bolted.

In terms of building the best models, the integration of financial statements is also crucial. An update to a revenue projection should automatically update gross profit, operating cash flow, and the ending cash balance. This avoids the pitfall of making changes to a part of the model without adjusting other parts, resulting in inconsistent outputs, which lack credibility with creditors and advisors. Being able to do this in a constrained timeframe is a sign of a distressed finance specialist.

Conclusion: Actionable Insights for Finance Professionals

Distressed financial modeling is a complex and high-pressure skill, and a distinction between general and specialist. It combines technical expertise in financial modeling with a comprehensive knowledge of capital structures and insolvency law, and professional judgement in dealing with uncertainty and time constraints. For professionals who wish to develop their skills in this field, the key to success for those just starting out or in the mid-career stages is practice, practice, practice; exposure to real-life restructuring situations; and a detailed understanding of the instruments of risk management and treasury management.

Start by getting proficient with the 13-week cash flow model. No other skill is more important in distressed finance. Once you can develop a forecast of weekly cash flows with appropriate supporting assumptions and sensitivity ranges, you will have the analytical skills that the advisors, creditors and managers care about most. Then develop your scenario and sensitivity analysis, so that you can isolate the two or three key variables that will make or break the business and effectively communicate that to a lay audience.

On the technical front, take time to study the details of how debt instruments work – the mechanics of the covenants, the waterfall of payments and the rights of creditors in a default. This enables you to turn your modeling from a number-playing game to a legal analysis that can inform the restructuring process. Read case studies: the Chapter 11 cases of large US corporations, the out-of-court restructurings in the leveraged loan market in Europe and the administration proceedings in the common law jurisdictions all have valuable lessons that can’t be learned from textbooks alone.

Lastly, work with the uncertainty associated with financial models of distressed companies. We are never going to know the future, but we are going to know the set of possible futures, and the best that can be done to assist decision-making is to give the decision-maker as clear a picture as possible of the risks and opportunities. A model that does this – that is open about its assumptions, robust in its calculations, and realistic in its caveats – is a very powerful corporate finance tool. When used by an expert, it not only sets out the facts of the distressed firm. It helps determine the future.